Geopolitical Risks in Technology Supply Chain

Since the publication of the Technical Standards at the end of 2012, market participants have started tailoring their projects and action plans in order to comply with EMIR's requirements.

After the long wait for the final EMIR draft language, the implementation challenge has become a race against time.

The timely confirmation requirement went into effect on March 15, 2013. As part of this requirement, Interest Rate Swaps (IRS) and Credit Default Swaps (CDS) that are transacted with financial counterparties must be confirmed by the end of the second business day (T+2), and IRS and CDS transactions with non-financial counterparties must be confirmed by the end of the fifth business day (T+5). For all other classes, swap trades must be confirmed before T+3 if the counterparty is a financial entity, and before T+7 if the counterparty does not fall within the definition of a financial entity. The confirmation window for all OTC derivative contracts will be reduced progressively to reach the target values by September 1, 2014: T+1 for financial entity counterparties, and T+2 for non-financial entities.

In addition to the timely confirmation requirement, EMIR imposes a separate requirement on institutions that trade swaps to report swaps data to registered Trade Repositories. The Technical Standards state that the reporting obligation for IRS and CDS should commence on July 1, 2013 and that the reporting of derivative contracts in all other classes is expected on January 1, 2014. However, the reporting obligation cannot be effective until Trade Repositories have been registered with ESMA.

Trade Repositories have started to apply for registration. The registration process is expected to take three months, and the obligation to report goes into effect three months after registration is complete. This places the date for mandatory reporting of IRS and CDS around September 2013, and January 2014 for all other classes of swaps.

Unlike the trade repository reporting requirement, the OTC clearing obligation will not impact institutions as quickly. This longer time frame is partly explained by the fact that CCPs must be authorized by their national authority or recognized by ESMA if they are not in the European Union.

The CCPs are required to apply for authorization / recognition before September 15, 2013 and the process is expected to take a few months, at the very least. Only after a CCP is authorized to clear a certain class of OTC derivative will ESMA make the determination as to whether that particular class should be subject to the clearing obligation (which may take an additional few months) and, if so, specify the requirements and the required compliance date.

The first clearing obligation under EMIR will most likely involve OTC derivatives for which there are existing clearing services, such as standard IRS and CDS that are currently required to be cleared under Dodd-Frank. The EMIR requirement is not expected to go into effect before 2014.

In addition to the requirements discussed above, the Technical Standards establish clearing exemptions for non-financial counterparties. A non-financial counterparty is exempted from clearing if its positions remain under the "clearing threshold." This threshold is determined in gross notional value and defined by class of swaps: EUR 1 billion for OTC credit derivatives; EUR 1 billion for OTC equity derivatives; EUR 3 billion for OTC interest rate derivatives; EUR 3 billion for OTC foreign exchange derivatives; and EUR 3 billion for OTC commodity derivatives. OTC contracts that hedge risks directly related to commercial activity or treasury/funding are excluded from the calculation of the threshold. If a non-financial counterparty exceeds a threshold in one class, then the clearing threshold is considered breached for the entire OTC derivatives portfolio and the counterparty is no longer exempted and must clear all swap classes.

With regard to CCPs, the Technical Standards define a framework to calculate the initial margin for centrally cleared OTC derivatives (a market risk model based on historical data), and the minimum parameters that must be used in this calculation. There are three factors considered. First, the confidence interval must be at least 99.5%. Second, the time horizon for the calculation of historical volatility cannot be less than 12 months and must include periods of stress. And third, the liquidation period shall be at least 5 business days. The Standards also establish the eligible collateral (cash, risk-free financial instruments, fully-backed bank guarantees, and gold) and the principles for collateral valuation and haircuts.

Finally, the Technical Standards provide operational terms (frequency, timing, thresholds, etc.) for portfolio reconciliation, portfolio compression, and dispute resolution. Institutions will have to periodically reconcile their OTC contracts with their counterparties, on a frequency varying between 1 day and 1 month (depending on the number of OTC contracts with the counterparty). In addition, institutions having a portfolio of at least 500 non-centrally cleared OTC contracts will have to set up procedures to analyze the possibility to conduct a portfolio compression exercise at least twice a year.

The Standards also provide the relevant effective dates (September 2013).

As for the collateral requirements for non-centrally cleared OTC derivative contracts (which is, as discussed above, one of the major implications of EMIR), additional Technical Standards are expected in 2014. These additional Standards will likely specify the precise level and exact type of collateral required. Until this second set of Standards goes into effect, counterparties will have the freedom to apply their own rules to their non-centrally cleared swaps.

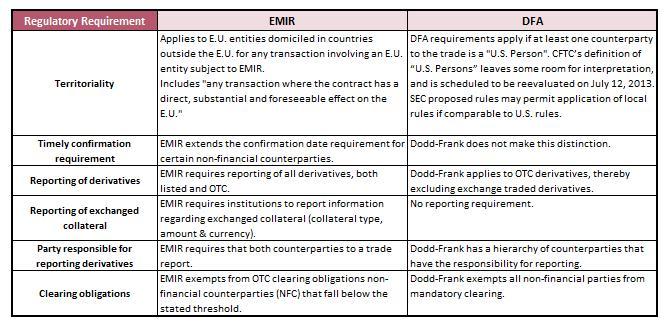

For many banks with a presence in both Europe and the United States, the compliance challenge is compounded by the requirement to satisfy both the Dodd-Frank and EMIR regulatory regimes. Astute and sophisticated firms should be able to exploit the synergies that exist between the regimes and reduce their compliance costs. However, significant differences between the two regimes should be noted:

Without a doubt, the United States has its own challenges and difficulties with multiple regulators and the potential for inconsistent of OTC derivatives regulation. This has the potential to drastically raise the cost of compliance for U.S. firms. In comparison, however, the European regulatory path has been longer and just as tough. Now that the regulatory process seems to be reaching its natural conclusion, the regulators' next challenge will be establishing a global regulatory framework by removing inconsistencies between borders and taking a common approach on territoriality questions.

To build the financial world of the future, there simply is no other option. Without fair economic and consistent rules at the global level, U.S. and European markets could become less competitive compared to non-regulated markets, and the mistakes and excesses of the past could arise again.