Carbon Accounting Management Platform Benchmark…

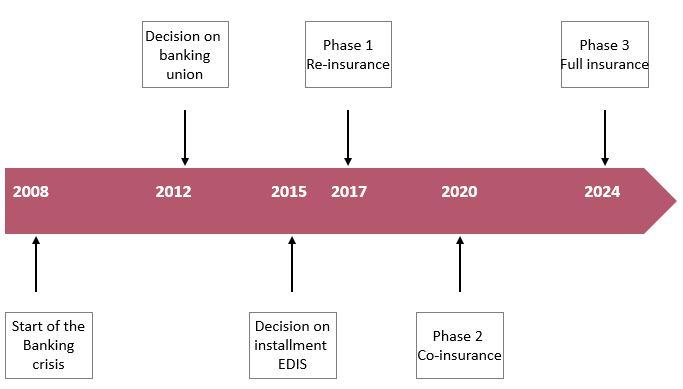

Almost 10 years after the start of the financial crisis that resulted in bank runs and the failure of several European banks and left millions of Europeans with empty deposits, the European Union has found an EU-wide solution to tackle future financial shocks and to protect deposits of citizens.

On June 22nd 2015, the “Five Presidents’ Report”of the European Commission decided to initiate a European Deposit Insurance Scheme (EDIS) as the finalization of the third pillar of the European banking union. EDIS will be put in place to guarantee depositors throughout the EU a 100,000 euro security on every deposit, a measure now put in place by deposit guarantee schemes (DGS) on which Sia Partners already reported in the beginning of 2015.

Since DGS are currently put in place individually by the European Union member states, there was previously no EU-wide solution for guaranteeing European depositors when banks across the Union found themselves in trouble. In order to meet these requirements and to strengthen the European monetary union, EDIS will be introduced on a step-by-step basis starting in 2017, finalizing in 2024.

This installation of the third pillar, officially proposed on the 24th of November by the European Commission, should strengthen confidence in the banking industry in Europe and take further steps in completing the European monetary union.

The European banking union aims to diminish the link between banks and national states. The past banking and sovereign debt crisis has shown the vulnerability of the system due to the vicious circle between sovereign debt and bank balance sheets. In order to meet this goal, the European Union has begun installing two mechanisms to establish the European banking union. The first pillar was the Single Supervisory Mechanism (SSM) to ensure homogenous supervisory standards across the European Monetary Union (EMU) while the second pillar, the Single Resolution Mechanism (SRM) aims to ensure the management of the resolution process for troubled banks.

In cooperation with these two pillars, the European Union is now adding a 3rd pillar. With the installment of EDIS, the European Union aims to disconnect balance sheets of their banks and their sovereign governments. The European banking union is in the first place mandatory for the countries that are part of the Eurozone (19 member states), as well as for all the European Union states that deliberately want to be part of the banking union.

This third pillar further strengthens the EU’s mission of creating an economic and monetary union, a long-term goal set back in 1991 during the treaty of Maastricht. In particular, this 3rd pillar fulfills one of the five criteria set forth by the European banking union: single rules and supervision of financial institutions within the euro area.

The European Deposit insurance scheme is the last step in fulfilling the European banking union. By 2024 this new system will replace the present deposit guarantee schemes which were put in place locally by the respective national governments, without fully removing them. EDIS will exist on top of DGS. The European Commission communicated that the installment of EDIS will go through three different phases of development over the next eight years.

First, it will start off with a re-insurance scheme to be introduced in 2017 next to the existing DGS. In practice this means that, in case of a bank crisis, the national deposit guarantee schemes would take action and start paying back depositors their guaranteed 100,000 euros per bank deposit account. When these deposit guarantee schemes are depleted, EDIS would add the balance of money guaranteed. In this first phase the importance of national deposit guarantee schemes is consequently larger than the involvement of EDIS.

A second phase will be introduced in 2020. EDIS and the DGS’s will complement one another. In case of bankruptcy, EDIS will contribute to the repayment of depositors starting from the first euro of loss. This system of co-insurance should start diminishing the importance of the national deposit guarantee schemes and the give more strength to EDIS.

Finally, the third and last phase of full insurance will be put into action in 2024. At that moment EDIS will entirely take over the roles of national deposit guarantee schemes and will insure them for the full 100%. While the DGS would stay in place, EDIS will be added to the present system. This would mean that the importance of EDIS would gradually increase over the years and diminish the role of the national deposit guarantee schemes in order to provide more safety and security to European deposit holders. By the end of 2024, this system aims to cover 0.80% of all deposits in the Euro-zone with a total of over 50 billion euros.

As of the beginning of 2016, banks should still be making contributions to the national deposit guarantee schemes until mid-2017. From then on EDIS will take effect and banks will start making contributions directly to the European deposit insurance scheme.

EDIS asks for the contribution of the banks that are located in one of the member states of the Eurozone (19 countries), though other states of the European Union can contribute to the European Deposit guarantee scheme as well. One of the major hurdles EDIS may encounter is the fact that Germany is not in favor of saving banks in other countries with money contributed from their own banks. As risk pooling is important in the Eurozone and in the European Union, Germany strongly believes that improving the banks’ robustness is the first main priority. As the most important economy in the Eurozone, the contribution of Germany to the proposal of a European deposit insurance scheme is crucial. Furthermore, the European parliament and a majority of the 28 member states of the European Union should give their approval before the installment of EDIS effectively takes place.

In addition, the introduction of EDIS also raises questions about moral hazard among the banks in the European Union. If banks will be backed by an EU wide system guaranteeing them instead of just relying on the limited national deposit guarantee schemes, chances rise that banks will opt for more risk in their investment. This can eventually lead to the banks’ collapse during financial shocks, as well as when depositors ask for their money back.

Lastly, the transition period from re-insurance to full insurance imposes a possible problem on the contributions of banks. According to the directive (2014/49/EU), DGS should guarantee 0.8% of the deposits of banks that fall under that DGS, getting to that level over a period of 10 years. This means that by 2024, the start of EDIS, national DGS should have reached that significant level. That is also the main requirement to get support by EDIS in case of emergency. If a DGS has not been able to raise the sufficient amount, it cannot count on EDIS support. In order to reach the specific amount of protection of deposits set by EU-law, the participating banks should make ex-ante contributions which are linked to the amount of deposits the bank is holding and determined according to their risk profile. The system of national DGS entails that the contributions of a bank are compared to another bank under the same DGS and the amount to contribute is based on the criteria described above.

Once EDIS will go into effect, banks will be compared based on deposits and risks profile to other banks EU- wide. The situation can occur that a bank then will have to pay more under EDIS than it did under the DGS. This can lead to discussions and the slowdown of a smooth implementation of EDIS.

A year ago, Sia Partners reported on the installment of the third pillar through the national guarantee schemes. Why does the European Union now need to introduce EDIS as the real fulfillment of the third pillar of the European banking union? Is there actually a need for the installment of EDIS?

One of the main reasons for the introduction of EDIS is the stability of the system in both the short and the long term. In case of bank failure today, DGS would take action and make sure that deposits worth 100,000 euros would be insured so that depositors are not carrying the mistakes made by the management off the banks. The problem with the DGS is that large local shocks cannot be fully supported. This implies that a failure of the banking system affecting multiple banks could be fatal for the present guarantee schemes.

Furthermore, an installment of EDIS gives a clear sign to the European citizens that there is something greater behind their deposits than just a national guarantor. Indirectly EDIS aims to restore the confidence in the European banking system and strengthen the effect of the two other pillars.

Overall it is definitely a step in the right direction to install EDIS by a gradual step-by-step process and to communicate a strong message to the European deposit holders. This process will allow the European Commission to deal with possible pitfalls that will occur down the road, optimize the EDIS construction, and prepare for different scenarios.

We are definitely not there yet and the European banking union still has some way to go, not only with guaranteeing depositors but also with the other two pillars. Pillar three is only one of the three pillars forming the banking union. In that way guaranteeing deposits goes hand in hand with strengthening the robustness of the banks and monitoring their behavior, in order to avoid dealing with bank failure.

It is only through the continuous optimization and monitoring of the three pillars that the banking union will be fortified and definitively installed. The EU will then be able to move towards a strong banking union that will be part of the European monetary union.

Copyright © 2016 Sia Partners. Any use of this material without specific permission of Sia Partners is strictly prohibited.

Please find here the full version of the article for futher reading.