From Data/AI Literacy to Fluency to Culture

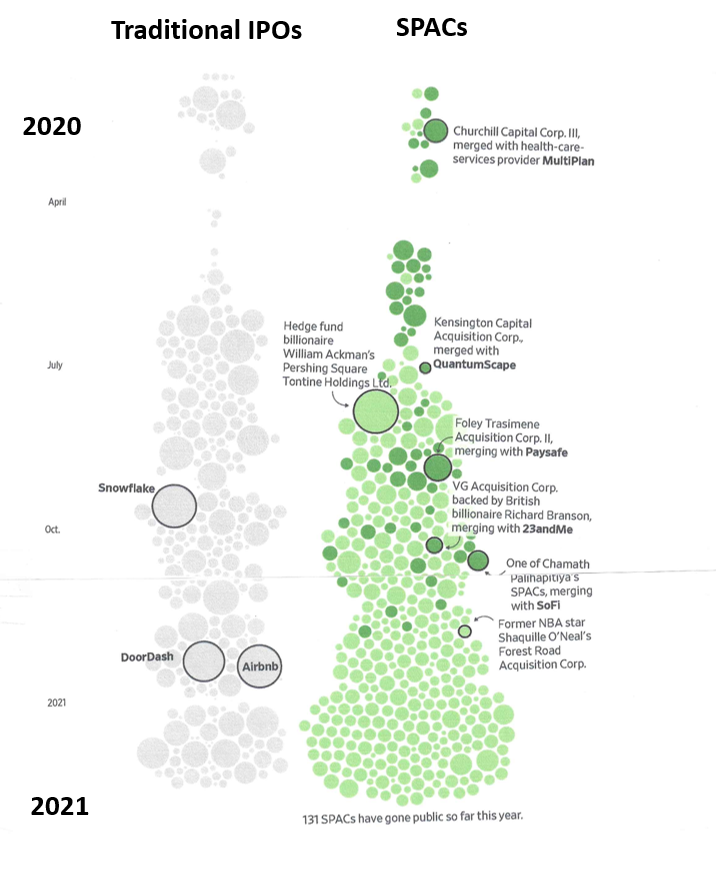

What is a SPAC? Volumes of these deals have exploded in 2020 and into 2021, potentially bringing lots of new early-stage companies to market. How do these deals work? What are the deal economics, and what are the implications of this boom?

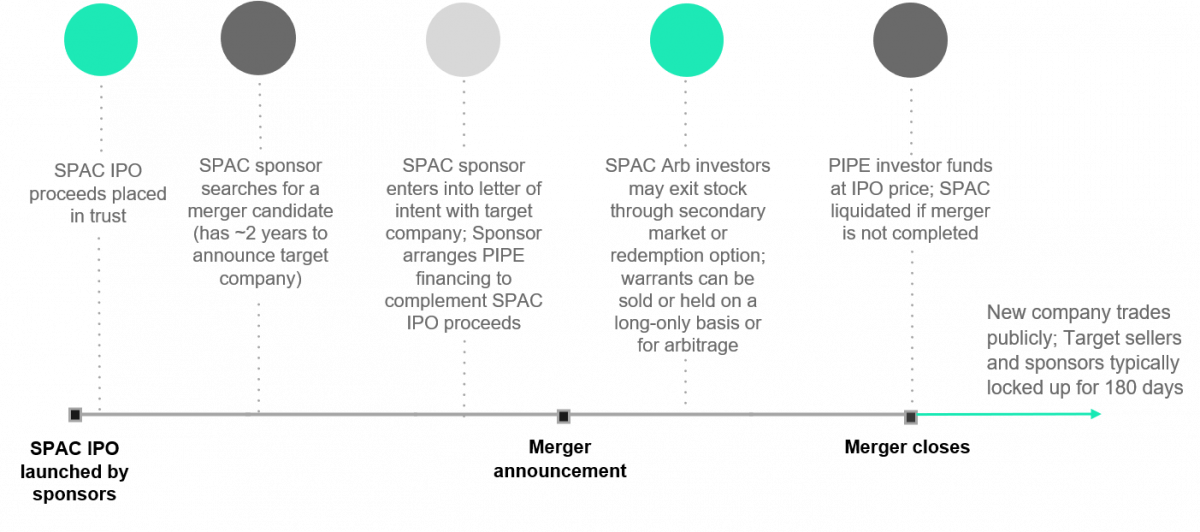

A SPAC, also known as a “blank check company”, is an alternative to the traditional IPO process to bring companies public:

SPAC Timeline: 2 Years to Find a Merger

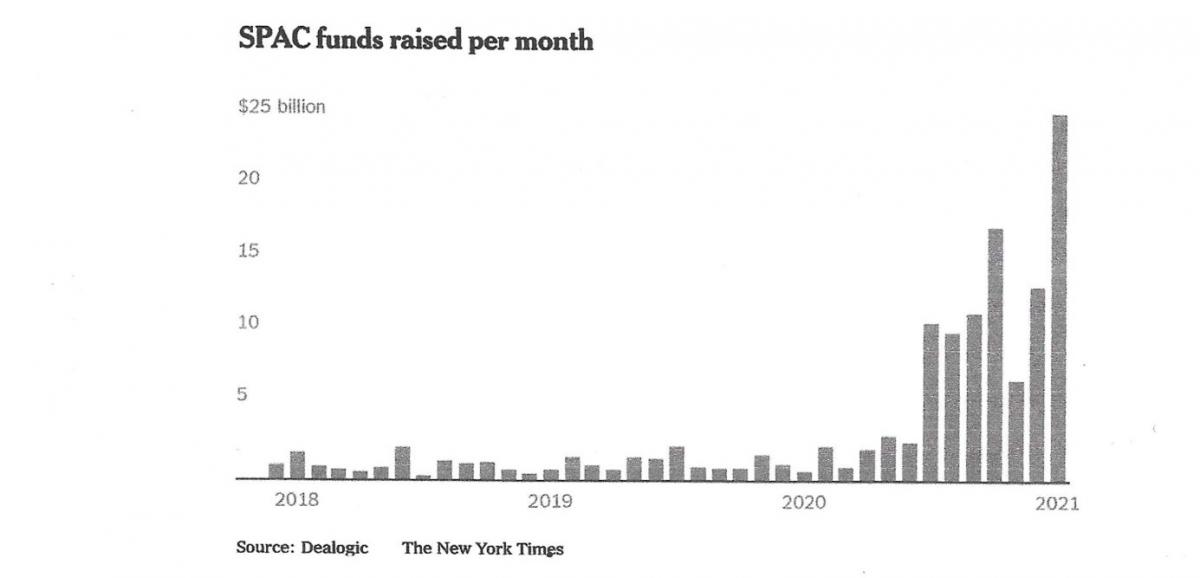

SPAC deals have been a small corner of the IPO market for years, but in 2020 volumes exploded to $82bn, nearly half the IPO market. The growth has accelerated in 2021, with $46bn raised through February 12th.

The overwhelming majority of recent SPAC deals have yet to announce or close mergers: approximately $100bn of SPAC issuance are looking for companies to acquire. Since SPACs can leverage themselves 3 to 5 times with PIPE funds, this implies $400bn or more of buying power.

SPAC deals are attractive to companies because of faster time to market, less disclosure and regulation, and less “money left on the table”. Per JPMorgan Research (“Eye on the Market”, Michael Cembalest, 2/1/21), which analyzed 85 completed SPAC deals and 5 SPAC liquidations, these deals are also very attractive to SPAC Sponsors, with extremely high returns. Other investors have had, on average, positive returns, but less than the IPO index or the Russell 2000. In all cases there was a wide dispersion between the most and least successful deals.

Sponsors: typically receive 20% of the IPO shares for a nominal amount, against which they have the expenses of the IPO including underwriting fees of circa 2.5%. They may have to pay “concessions” to PIPE investors to enable the deal to close. Estimated median return was 418%, assuming 25% concessions.

IPO investors; typically receive shares plus warrants. Estimated median return was 45% if shares redeemed pre merger closing, and 8% if held more than 180 days post merger (deal “seasoning period” after which merger insiders and IPO Sponsors are permitted to sell their shares).

Pipe investors: receive shares plus “concessions” from the Sponsor. Estimated median return including concessions was 41% if shares redeemed pre merger closing, and 13% if held more than 180 days post merger.

Note that these returns are for completed deals—and the overwhelming majority of SPAC deals brought in 2020 and 2021 are as yet uncompleted.

To some commentators, the flood of SPAC issues is a sign of market speculative excess, similar to the dot com boom (and bust) of the late 1990s, where unproven companies were brought to market at extreme valuations.

To others, SPAC issuance is now a major permanent factor in the IPO market, providing issuers with faster completion of deals, greater flexibility in financing structures, and greater certainty of issue proceeds. Initial and PIPE investors get access to Private Equity and Venture Capital deal flow, with principal protection and an equity upside.

What is clear, is that there is a major misalignment of incentives between deal sponsors and end investors. Sponsors stand to make money in almost all deal outcomes, with huge upside in the most successful deals. Per Bill Ackman, “People used to say that hedge funds are a compensation scheme masquerading as an asset class…You could say the same about SPACs.” Post acquisition SPAC returns have trailed far behind both traditional IPOs and the broader market.

Likewise, PIPE investors, with the option to redeem their shares plus interest, have the ability to earn a positive return in almost all deal outcomes, plus substantial upside in the most successful deals.

Some market participants see the potential for major market disruption, as happened in the dot com saga. Others point to imbalance between funds chasing merger deals and the supply of quality merger candidates. With the large and growing number of SPACS yet to announce or close mergers, and as deals get closer to the two year deadline, there will be pressure to do a merger at any price, rather than return money to investors.

John Gustav

Partner

+ 1 (516) 810 8719

John.Gustav@sia-partners.com

Joseph Willing

Managing Director

+ 1 (347) 380 3960

Joseph.Willing@sia-partners.com

Danielle Fair

Manager

+ 1 (267) 614 2703

Danielle.Fair@sia-partners.com

Zoya Ashirov

Managing Director

+ 1 (917) 330 5536

Zoya.Ashirov@sia-partners.com