Canadian Hydrogen Observatory: Insights to fuel…

August 25th, 2017 | Hong Kong.

Our distribution tour continues with Edward Moncreiffe, CEO for Hong Kong at HSBC Insurance (Asia) Limited. We have had the opportunity to explore the following topics:

Can you describe your role within HSBC?

I am the CEO for HSBC Insurance in Hong Kong. We are the leading life and pensions provider in Hong Kong, and as a bank we are one of the largest distributors of general insurance in Hong Kong.

Where do you see insurance distribution going in Hong Kong and Asia?

Hong Kong is fascinating because it is a developed market, with one of the largest penetration per capita and yet it is still one of the fastest growing insurance market in the world.

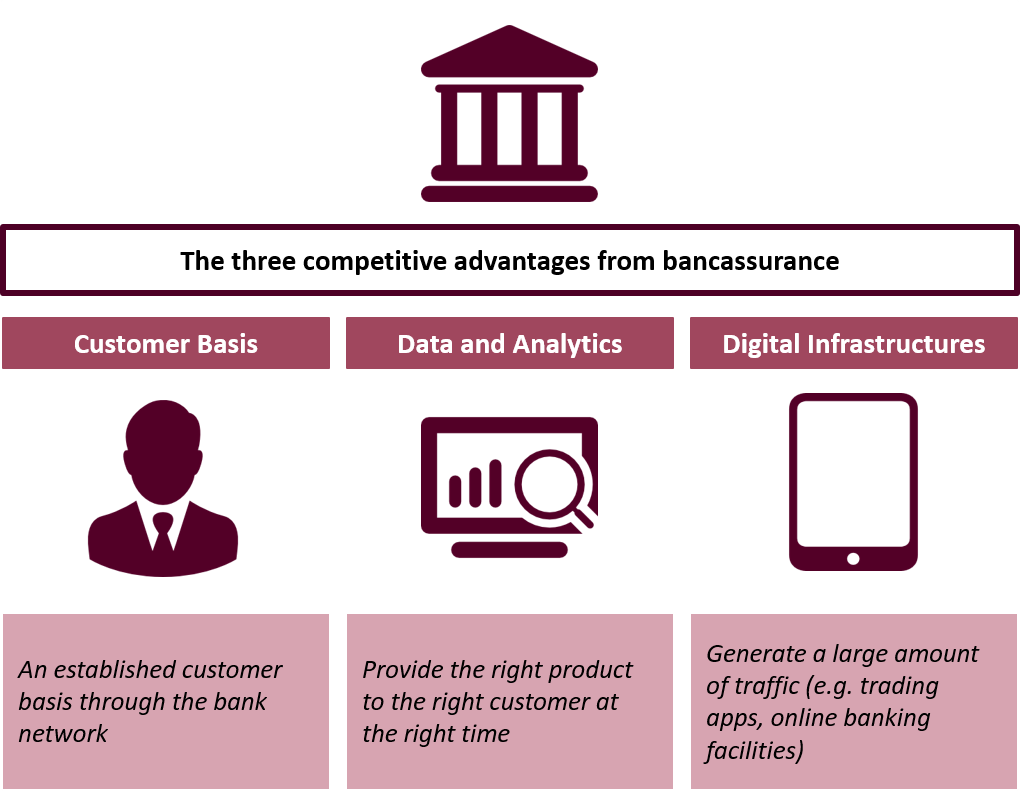

Bancasurrance is responsible for the majority of our revenue in Hong Kong. It will continue to be a dominant source of distribution in Hong Kong, because banks have three competitive advantages over insurers:

Additionally, digitization is going to be very important. A year ago we did not have any online life insurance business, now 7% of our business come from digital channels in terms of case count. I think we are only touching the surface of what can be achieved.

Another change will be in the broker space, as the definition of a broker continues to broaden along with the changing regulatory landscape. We need to ensure we partner with the right entities for the right type of product.

How does HSBC differentiate itself in distribution?

Our extensive distribution channel gives a much wider understanding of our customers’ needs, goals, or even dreams at any point in time. We can also offer a much larger set of products from the bank side, which is outside the classical insurance product list. As a bank we also tend to keep long term relationships with our customers, therefore we have a more comprehensive approach to offering insurance with our customers.

On the longer horizon we intend to differentiate by making bancassurance more using two streams of improvement:

What is your target distribution mix for products and channels?

We do not have any target for distribution mix and as a group we do not provide for any individual product target. The reason is because this can create misconduct issues, similar to the one banks and other financial institutions experienced in the 1990s.

We sell to need! In that sense we have produced comprehensive frameworks in order to clearly define the needs of our customer and map them to a customer journey such as protection, education, managing wealth, retirement and legacy planning.

How do you manage the multiple channels available for the distribution of insurance products?

Historically insurers worked with channels in silos, which can bring positive income in term of competitive instinct between them, however it can also create a negative reaction as you cannot build synergies if you assume the customer will stay in the same channel.

That is why we invest heavily in multi-channel capabilities.

We should not consider a customer only inside one branch, but rather see the potential cross pollination between channels.

Does HSBC size brings more complexity in achieving cross channel capabilities?

It is true that HSBC is a very large organization, and large organizations can pose challenges in implementation in term of strategic thinking and deployment. However once we manage to implement our initiatives the benefits and potential are multiplied.

I believe we created an organization that not only reward its sales operations based on the revenue they generate but rather on the value they add to the organization, and we managed to take this cultural transition successfully.

In order to achieve these capabilities, do you invest in cultural transformation programs?

Absolutely, HSBC Group takes conduct risk extremely seriously. We have spent more than a decade managing and improving our conduct risk framework, including cultural trainings and frameworks for our staff. I think conduct risk is probably the single largest emerging risk for Asian insurers.

Point in sale transparency is also extremely important in order to make sure we sell insurance and respect these four principles:

That is one area in Asia that we want to improve significantly, having gone through this journey in other parts of the world. For example GN16 is a regulation which we are hugely supportive of, as it creates a much greater level of transparency from the insurer to the customer at the point of sale and on an on-going basis.

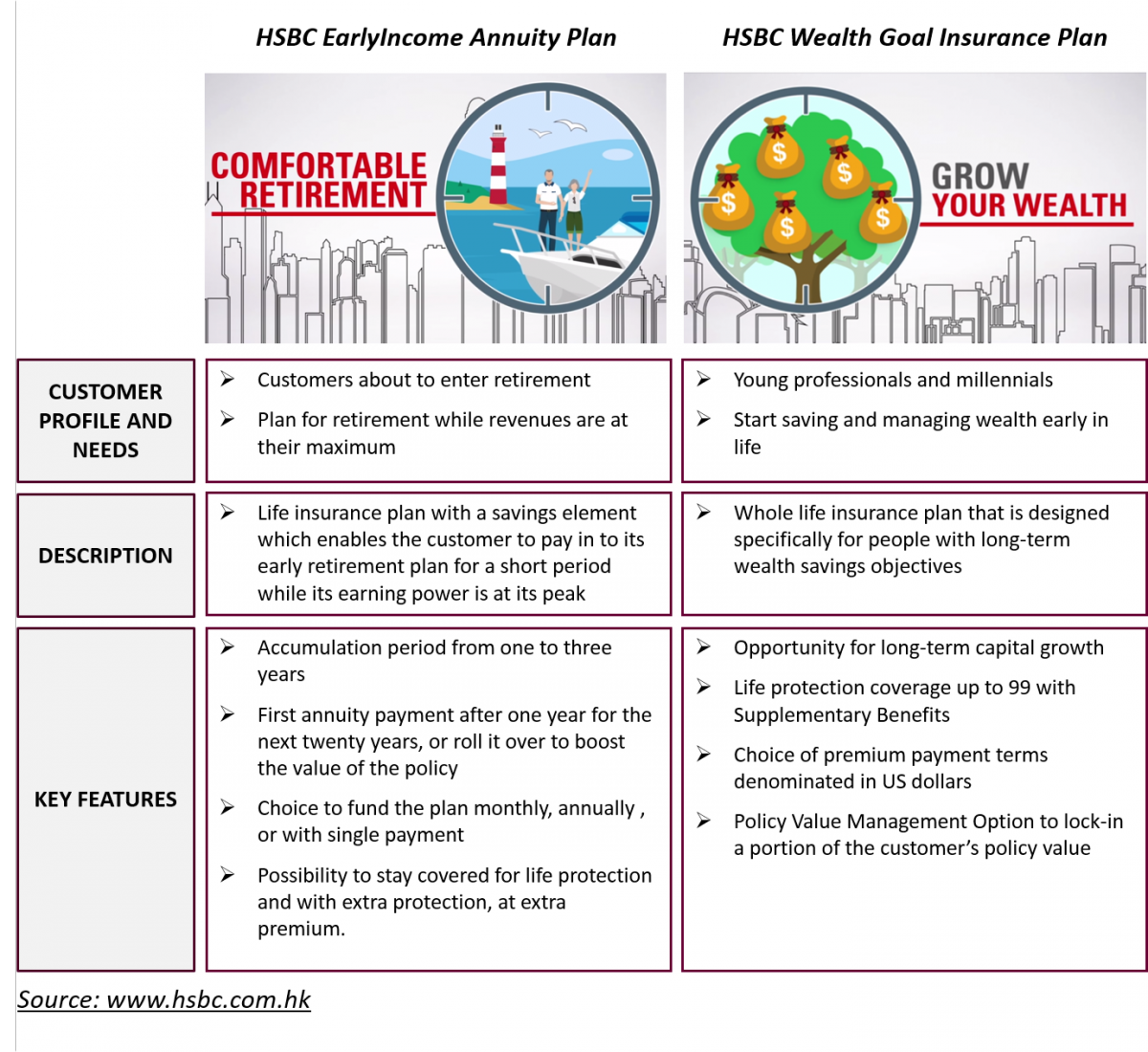

How does HSBC capture the “silver age” and millennial opportunities in Hong Kong?

The silver hair market is strategic for us, especially now since Hong Kong women have the longest life expectancy in the world. We have invested a lot in products such as retirement (e.g. liquidity replacement), income replacement, long term care and medical support.

We also re-launched our flagship retirement product called EarlyIncome Annuity Plan, which provide annuities and significant guarantees for customers as they enter retirement.

As for millennials, we designed a product called HSBC Wealth Goal Insurance as these customers need to save more and earlier because they may not have the favorable economic situation that their parent had.

What is HSBC working on in the digital distribution space?

We work differently according to the type of insurance.

The challenge now is to turn on our mobile environment into an “always-on” environment. As millennials start to penetrate the market, we have to be quick, always on and incredibly accessible. This will be key not only from a sales perspective, but also from a servicing and claim perspective as well.

For the Life Insurance business, the complexity of products and the regulatory environment has always been a constraint to digitization.

We launched our fully online first term life plan last year, using a straight and simple process to strip out the variants so that it can be accessible to everyone in a few minutes. Today in HSBC you can buy a 5,000,000 HKD term life insurance policy in only five minutes. And we will do much more than that in the future. This will probably involve and lot testing and failing, but eventually that is how we will be able to lead the market.

On a longer term, we will need to transition into more hybrid products such as savings. For now it is very easy for a customer to go online and buy for example risky emerging market bonds or US equities, while it is still difficult to get life insurance. We have to change that.

Can AI play a role in helping customers choose the right products, similar to roboadvisors?

AI drives our digital agenda, as we want to be able to understand the customer buying and browsing habits. One the robotic piece, we are targeting to grow into a more sophisticated personal advisor concept for the longer term.

However, I do not think we will completely dehumanize insurance, as the Asian insurance industry relies on face to face interaction. The strength of the human relationship will never be 100% replaced. As at HSBC customers are at the center of what we do, face to face interaction can let us better understand our customers and allow us recommend products that are tailored to their needs. But for younger generation that are more familiar with online purchase, the company that has the best AI and analytics capabilities will definitely get the bigger size of the pie.

Regarding new market entrants in digital distribution, would you consider them as are a threat, a motivation to push yourself or a pool of potential partnerships?

We consider them under these three angles:

An example, we launched an initiative in partnership with Prenetics in Hong Kong called “ONEdna”.

It includes a simple saliva test for screening DNA which provide a comprehensive report for the customer to know DNA affects its health risk, nutrient absorption, drug response, and risk of common cancers. This data can be linked to a HSBC protection plan, and we offer monthly reward such as premium discounts for ONEdna customers through the application. This data can be linked to 6 HSBC protection plans.

What does your DNA says about?